Events of the past few years have resulted in a significant increase in demand for ESG (environmental, social, and governance) data. Between heightened climate change advocacy, increased attention to natural capital and biodiversity risks, scrutiny on social issues such as racial injustices and inequalities, and the evolution of regulations and standards, need and opportunity for ESG data has exploded.

Requirements for more transparency into business conduct have resulted in greater demand for more actionable, relevant, transparent, and standardized ESG data. With this increased demand comes increased supply. With more opportunity to supply, vendors need to stand out and innovate to meet the evolving and ever-increasing requests from the industry. But does this lead to confidence or confusion? How can education of market participants support clarity around ESG data and better decision-making? How has the influence of government, regulators, stakeholders, and society played into the evolution of ESG data and technology, and how are vendors coming together to bring innovation into the ESG space?

This paper explores the evolution of ESG data and its future potential, with a specific focus on how strategic partnerships between service providers are changing the landscape of opportunity, and with contributions from our partners at Qontigo, ICE, and K2 Integrity.

I. The current ESG landscape

The roster of ESG (environmental, social, and governance) data and technology providers is forever expanding. With a remit to solve for the complex use case of ESG material impact and performance, alongside encouraging responsible business practices, vendors are looking for opportunities to close data gaps surrounding ESG assessments. For their clients, whether assessing their own impact, understanding the ESG risk profile of a counterpart through traditional Know Your Customer (KYC) or due diligence activities, reviewing supplier or merger and acquisition (M&A) targets, managing ESG risks through portfolio and investment screening, or analyzing responsible consumer practices, ESG data and technology are a driving force for uncovering risk and opportunities.

Analysts at Opimas1, a management consultancy focused on global capital markets, reported that the ESG data industry (research, analytics, and indexes) exceeded USD 1 billion for the first time in 2021, with an annual growth rate of 28% over the past 5 years. The ESG data market was expected to exceed USD 1.3 billion in 2022 and to grow to over USD 5 billion by 2025. Meanwhile, the ESG software market, valued at USD 489 million in 2020, is projected to reach approximately USD 1.5 billion by 2028.

The report also found that ESG data spending was estimated to have grown by 39% in 2021 and 24% in 2022, and was driven by EU regulatory requirements around ESG disclosure and climate risk, as well as increased investor demand to incorporate ESG risk in investment strategies.

Regulation across borders has advanced to include ESG-related disclosures and due diligence assessments and has influenced the direction of ESG integration: in Europe, the Sustainable Finance Disclosure Regulation (SFDR) and EU Taxonomy Regulation; in the United States, proposals for enhanced climate risk disclosure requirements and Nasdaq's Board Diversity Rule; and in Asia Pacific, new taxonomy frameworks and initiatives like the Green Finance Action Plan and the Green Finance Industry Taskforce (GFIT).

External requirements and internal strategies must be supported by the right ESG data and technology for effective and efficient execution. The evaluation of vendors by firms can be complex, and decisions are being delayed by lengthy assessment cycles. The number of ESG data and technology options available on the market today and the many factors that define a good ESG data solution, continue to contribute to the complexity in finding the right implementation.

II. Moving away from traditional approaches

Traditional ESG ratings providers have substantial penetration of the ESG data market today. Many rely exclusively on company disclosures to inform sustainability assessments. ESG ratings providers look at industry and sector analysis and often specialize in specific asset classes, providing ESG ratings that enable firms to benchmark and compare companies based on their self-reported data as well as conduct bottom-up sector and company ESG materiality analysis. Most providers are heavily geared towards the public sector, while new players are attempting to close the gap and deliver solutions for private market participants.

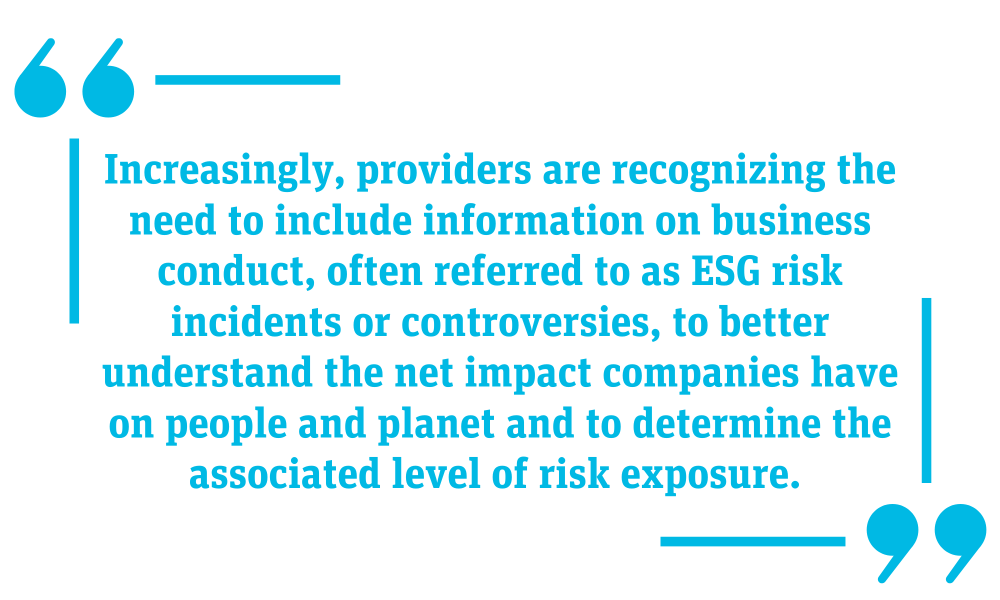

Increasingly, providers are recognizing the need to include information on business conduct, often referred to as ESG risk incidents or controversies, to better understand the net impact companies have on people and planet and to determine the associated level of risk exposure. However, challenges lie in the level of timeliness, granularity, and transparency of the information disclosed by companies, and suitability for due diligence and risk management purposes. Annual or quarterly updated data does not meet investors’ needs nor the pace of the global economy. In addition, it can be difficult for ratings providers to determine accurate ESG exposure due to the potential for bias in self-reported data, inadvertently masking underlying risks. Meanwhile, changing methodologies and variations in traditional ratings weightings and calibrations make it difficult to conduct backtesting and consistent analysis, effectively clouding the bigger picture.

III. The opportunity

Today, financial institutions and corporates are looking for alternative, complimentary, and innovative datasets to broaden their ESG risk assessments. With ESG encompassing a broad range of issues, and subject to multiple interpretations, vendors have an opportunity to develop datasets in a variety of segments, and by utilizing advances in technology to innovate on delivery.

Artificial intelligence, machine learning, and natural language processing are being used to increase scalability and speed of delivery for emerging data products. By establishing strategic partnerships and through M&A activity, a vast array of products and services are entering the competition for ESG data domination. Between 2010 and 2021, the industry saw the establishment of nearly 90 new ESG data and technology vendors.

The FTSE Russell 2022 Global Survey1 of asset owners, identified data availability, data standardization, and concerns about quality or consistency of corporate reporting and disclosures as being the main barriers to entry to increase sustainable investment adoption across all asset classes. Similarly, a recent global ESG market study2 from Northern Trust and PwC identified the collection and analyses of data as the top challenge for asset managers and asset owners.

Data is a challenge. The journey of realizing its full potential is a long one, but there are avenues of opportunity to explore.

IV. Data coverage and solutions

A report published by Substantive Research1 in 2021 looked at the specialization of ESG data providers, identifying that 53% of ESG data providers were looking holistically at all three pillars, 35% specialized in one of the three, with the majority (70%) focusing on environmental data. Influenced by society, consumer behavior, regulation, and government, data providers are developing specialized datasets to meet the needs of the industry.

In the last 19 years, ESG data science company RepRisk2 has evolved its research scope from 20 to 80 thematic tags to classify ESG risk-related incidents, with ‘Economic impact,’ ‘Health impact,’ ‘Land ecosystems,’ ‘Marine/Coastal ecosystems,’ Opioids,’ and ‘Salaries and benefits’ being introduced in the last two years. The main catalyst for this evolution is industry demand for greater thematic granularity, and demonstrates the adaptability of data and research vendors to deliver relevant information on an evolving, non-standardized ESG use case.

In 2008, RepRisk identified the most environmentally and socially controversial companies as those operating in the Food and Beverages, Oil and Gas, and Electronic and Electrical Equipment sectors. A decade later, the top controversial companies were operating in Industrial Goods and Services, and Chemicals and Healthcare Equipment and Services sectors. ESG issues such as ‘Human rights abuses,’ ‘Corporate complicity, corruption, bribery, extortion and money laundering,’ and ‘Impacts on communities’ were identified as the top three issues. Consistent methodology enables tracking of trends and making it possible to conduct backtesting.

The last 10 years – ESG data advances

Amid a new generation of ESG datasets and applications, there are advancements in data quality, types of metrics, and information sources.

In terms of quality, ESG datasets have become more granular, transparent, and in some cases market-specific. In addition, there are now highly specialized metrics focusing on topics like biodiversity, gender, and modern slavery. Specifically, for climate data, new types of metrics have emerged that can add accountability to forward-looking climate strategies – through information on CapEx, R&D investments, and even company patents. In addition, there is innovation in terms of how the data is sourced. As an example, the use of satellites is a novel way to obtain companies’ ESG data.

The last 10 years – ESG data usage

Investors’ sustainability objectives are becoming increasingly nuanced. There is a clear mindset shift for our clients. What was earlier a question of how they can improve their overall ESG profile, now focuses on defining specific objectives for their sustainable investments.

When it comes to how data is being utilized in more innovative ways, some investment products are now integrating over-time criteria, which incentivizes investee companies to have transition plans, instead of excluding systemically important companies based on point-in-time data. This is important especially in the context of net zero.

We are also seeing some exchange traded fund (ETF) managers incorporate engagement guidelines, combine forward-looking metrics, and even use non-commercial frameworks in investable products.

The evolution of industry assessment of ESG data and technology vendors

Data/technology vendors can be assessed in six areas:

- Material risks: how ESG scores reflect companies’ risks

- Opportunities: companies’ share of revenues in sustainability-related products and/or services

- Forward-looking indicators: R&D expenditure in sustainable products and services, green CapEx/OpEx, green patents

- Framework/legislation-related metrics: companies’ alignment with temperature trajectories, alignment with EU Taxonomy and SFDR requirements, biodiversity-related data

- Reporting: possibility to produce detailed reports, customizable according to clients’ needs

- Data feed: how data is delivered to clients, depth of historical data

V. ESG integration within organizations

ESG implementation can sit in many different areas of an organization and has recently pivoted to areas including legal and finance, introducing new dynamics to how and why ESG is considered.

In a 2020 report, Deloitte1 noted that ESG integration for chief legal officer could cover three key components: 1) communication of risk and opportunity on ESG strategy, 2) development of ESG reporting and disclosure mechanisms, and 3) influencing the regulatory environment.

KPMG2 highlighted the expanding responsibility of the chief finance officer to track and report on information needed for ESG strategies and relating this to data on sales, supply chain, customers, and other business areas. This extends to the need for more visibility at board level to identify key material ESG factors for assessment and decision making.

Another prominent area where ESG resides as an overlay is within the risk management function in an organization. Risk managers assess internal and external factors that can impact opportunities for a company, with results informing strategic and tactical business decisions. ESG data plays an integral part in the overall assessment of a company’s risk exposure, but with the wide remit of risk, there is never a single solution, and firms look to a multitude of data points to input into a risk management framework.

VI. Collaboration unlocking potential

Increasingly, decision-makers are realizing that no single ESG dataset should be used in isolation to solve for an ESG-based need. With increased scrutiny of ESG and more attention being paid to responsible business conduct, ESG data and technology vendors are being challenged to shed light on how companies are impacting society and the environment – both positive and negative impacts. One fast-moving and creative way the industry can do this is with effective partnerships.

A 2021 review by Ernst & Young1 identified that over 60 of the largest financial services firms across Europe and the US are using between two and five different data providers to cover their ESG needs, with some using up to 10. Firms are combining ESG data sources, methodologies, and analyses from different vendors, including traditional ESG ratings, sentiment analysis, regulatory coverage, and modeling.

Ernst & Young noted that ESG data vendor solutions were concentrated in three areas: measuring progress against the Sustainable Development Goals (SDGs), modeling net-zero commitments, and tracking greenhouse gas emissions.

Increased focus from regulators and stakeholders on net-zero and carbon reductions has led to a greater need to understand the absolute value of a company's footprint. Vendors provide solutions helping companies set emissions targets, monitor, report, and model their emissions data. The latest advancements in technology allow satellite-enabled data to track both negative and positive physical risks and impacts on the ground, including greenhouse gas emissions, deforestation, as well as tree planting and ecosystem remediation.

Geospatial proximity data enables the assessment of biodiversity risk by locating where infrastructure projects, such as mining and oil and gas sites, interface with environmentally sensitive sites. Such data feeds into ESG risk assessments in insurance underwriting and real estate and can help portfolio managers understand biodiversity risk across entire portfolios. Since 1900, the growth in the number of protected areas and Other Effective Area-based Conservation Measures (OECM) has increased on both land and water by 12 million km2 and 26 million km2 respectively, as reported in the Protected Planet2 2020 report. There are over 16,000 Key Biodiversity Areas in the World Database with over a quarter of these locations with identified threats. Access to this information can close the gap between the private sector and biodiversity conservation efforts, to help decision-makers understand and mitigate physical risk to the planet.

Solving for data challenges

The challenge with satellite data lies in mapping the information within the context of local market, policy, and geographical conditions. Specifically for emerging markets, many of the manufacturing, agricultural and production sites are run by smallholders operating in disorganized market conditions. An example would be measuring stranded asset risks based on:

- Each company’s sector, geographical location, and market conditions

- Real-time and predicted ESG performance

- Other asset-level information such as CapEx, and whether it is aligned with the low-carbon transition

We believe that satellite data could solve the biggest issue with net-zero targets, i.e., ‘time-washing’ – where companies setting long-term targets have little change to show in the short-term. Short-term changes can be a good indicator of a company’s intentions and a predictor of whether goals will actually be achieved. Satellite data can be very effective in measuring these changes and can be used to determine stranded asset, compliance, and reputational risks.

On the risk side, a more long-term example (one that would be useful but difficult to map through the supply chain) would be climate linked-physical stressors impacting profitability, cost of capital, or supply chains, including:

- heat index (impacting agricultural growth, worker productivity, real-estate prices)

- flooding and fire risk (impacting insurance prices, insurance gaps)

- water and other natural resource availability (impacting business processes)

To solve this, satellite data needs to be investor-friendly. A lot of valuable data currently exists in the academic domain that is not useful for investment products, specifically those in the passive-investing space. We have seen some promising start-ups taking up the challenging task of developing datasets for investment use cases. Industry push towards enhancing such research and development efforts could speed up the adoption of satellite data.

ICE, via its acquisition of Urgentem, has been collecting company level carbon emissions data for over ten years. During this time, we have witnessed a significant improvement of both the availability and quality of data. Our latest data assessment covering the 2021 ICE Emissions Dataset reveals a particularly positive trend regarding emissions disclosure and the quality of disclosure globally. Overall, our analysis of disclosures by companies in the ICE Emissions Dataset found that there was a 15% increase in public disclosure of climate data. Even more encouraging is the fact this improvement has been led by many companies providing comprehensive Scope 1 and Scope 2 emissions public disclosure for the first time.

In 2021, companies achieving ICE’s top disclosure quality rating (i.e., public disclosure of Scope 1 and 2 emissions covering at least 95% of a company’s operations with third party assurance) jumped by over 40% from the last reporting year. This increase includes companies improving their previous public reporting as well as companies who reported publicly for the first time.

But despite this improvement, data availability continues to be cited by investors as an issue. A recent survey commissioned by ICE and carried out by Coalition Greenwich (Expanding ESG Capabilities - Improving Data to Advance the Journey) asked global fixed income asset managers their views on ESG data availability. We found the results extremely interesting. While not surprised by the general view that ESG data is important (90% of respondents) and that more data is needed (85% of respondents), we were surprised by the asset classes where data availability was perceived to be most challenging. The asset classes cited, such as Municipal Bonds, are areas where data tends to be available and used within the financial industry. Our conclusion: more needs to be done to raise awareness of ESG data availability to counter this misconception.

Overall, we are encouraged by the extent to which participants in the fixed income markets view integration of ESG data into their investment decision-making process as important and cite the need for additional data and products to achieve this goal. This suggests ESG considerations may be gaining in prominence alongside traditional financial valuation, performance, and risk management related criteria in fixed income markets.

As a result, demand for the raw underlying ESG data is likely to increase to allow for more in depth analysis. The desire to move away from ESG rating and scores, suggests fund managers are differentiating at a more granular level and the data and tools to do so are now available.

VII. Impact of regulation

Regulatory solutions make use of self-reported data to support firms in the completion of various disclosures around the world such as SFDR. These solutions are mapped to regulatory frameworks, linking self-reported data fields to required disclosures such as those related to gender pay gaps, board diversity, and product marketing metrics. With regulation highlighting challenges around the standardization, interpretation, and availability of data, these tools serve to simplify the process and enable the reuse of information to create consistency and streamline reporting.

One development in this space is vendor partnerships that combine self-reported data with third-party data to provide an accurate assessment of a company – an assessment that is increasingly being required for reporting purposes. To get a true representation from a regulatory perspective, particularly with reference to due diligence, this outside-in perspective is fundamental in completing the picture.

Globally, policy makers and regulators in financial markets are adopting and implementing more stringent ESG and climate related regulation, with financial product classification and labeling currently under the spotlight. Generally, this is viewed positively by most participants. But are there unintended consequences to this increased regulation?

Financial product ESG labeling is a hot topic and as a result, ESG fund classifications are facing closer scrutiny. High profile fund reclassifications and downgrades (from Article 9 to Article 8) have been grabbing the headlines and sparking a debate as to the reasoning for these changes in classifications. One of the questions being asked is: Were these funds unable to stand up to the closer scrutiny that Article 9 classification brings, or are the fund managers just looking to avoid that scrutiny in the first place and avoid the burden of increased disclosure, willing to settle for a lower classification, especially given the focus on greenwashing in the media?

Our analysis of the ICE database on fund classification points towards a less cynical and more positive trend overall when it comes to the ESG ambitions of funds. While there has been a decline in the total number of funds with an Article 9 classification over the past year, with that decline accelerating in the last quarter of 2022, the overall direction of travel remains positive. The downgrades from Article 9 have been outweighed by upgrades to higher classifications elsewhere, especially with an increase in Article 8 funds. The bulk of this increase of Article 8 funds is the result of funds moving from an Article 6 to an Article 8 classification, rather than a downgrade from Article 9.

Overall, there appears to remain a trend towards achieving higher ESG classifications, even if the highest classification, Article 9, may seem less attractive to some funds given the associated restrictions, disclosure burden, and risks.

As highlighted in our recent blog, the most significant difficulty with ESG regulatory mandates (SFDR, MiFID) is that they provide a vague definition of sustainable investment, leaving the responsibility to Financial Market Participants (FMPs) to determine how to implement this broad concept in practice. In the past year, FMPs have put significant effort into developing a defensible interpretation of these regulations and into defining sustainable investments.

Further clarity is expected over the next two years. In addition, companies are stepping up the disclosure of key data.

At such a time, we would expect our data providers to ensure their dataset methodologies are updated alongside evolving regulation and to incorporate new information. Additionally, within the Principal Adverse Impact (PAI) indicators defined under SFDR, some metrics are yet to be widely collected at the corporate level. For example, for PAI 11, which identifies the share of investments in companies with due diligence processes to ensure compliance with the UN Global Compact and OECD Guidelines for Multinational Enterprises, data availability for approximately 11,000 companies considered lies below 20% among ESG data providers that we have assessed.

What would ease the burden is regulatory clarity on: (1) what constitutes a company’s positive impact through its products, services, and operations; (2) how sustainable investments can be aggregated at the fund level; and (3) what the qualifying thresholds are for specific metrics under SFDR PAIs/Taxonomy/MiFID.

Regulatory requirements related to ESG disclosures are just starting to ramp up. While the EU took the lead with the SFDR, the draft sustainability disclosure requirements being proposed by the UK FCA and labeling requirements proposed by the US SEC make clear that global regulators are not done. The risk of contradictory or competing guidance goes up exponentially as the number of regulatory bodies and jurisdictions with their own set of ESG requirements increases. Compliance teams can often feel overwhelmed just staying up to date on current requirements, let alone integrating new ones.

Short of a global convergence of regulatory requirements, firms need to establish flexible processes that will allow them to collect and report on a variety of metrics across different contexts. Most importantly, firms must be able to “show their work” and demonstrate that they are using quality data in consistent, defensible processes.

The best way to avoid claims of greenwashing now or in the future is to be clear about how both the spirit and the letter of the law are being met. Where assumptions, estimates, or otherwise imperfect data must be used, firms should be clear about the existing limitations and why the approach they are taking is reasonable.

A culture of continuous improvement and self-reflection is also important to ensure that a firm’s approach does not become stale over time. As additional data providers come online and existing data providers extend their product suites to fill market needs, firms should look for opportunities to transition from broad estimates to exact data wherever possible. Change is always difficult but the ability to confidently know that you are meeting regulatory expectations is worth it.

VIII. Impact of misleading communication and greenwashing

One of the most prevalent grievances in ESG is about greenwashing, with some major financial players being hit with investigations following accusations of miscommunications and misconduct on their ESG claims. The Securities Exchange Commission (SEC) has begun to increase their scrutiny of sustainable investing claims with a USD 1.5 million fine to BNY Mellon in May 2022 following misstatements and omissions about its ESG approach to managing funds, and a USD 4 million fine to Goldman Sachs in November 2022 for ‘several policies and procedures failures’ involving ESG research. The Australian Securities and Investments Commission (ASIC) issued their first greenwashing fine to Tlou Energy in October 2022 citing four infringements for making alleged false or misleading sustainability related statements. It is clear that regulators are closing the margin of error for what firms are publicly declaring regarding their ESG credentials.

Auditing combined with better data and technology is a strong partnership for the industry. By combining expertise to uncover any discrepancies in assertions, firms can take an external perspective on their ESG claims, adding to effective processes and procedures when it comes to due diligence of marketing claims. These types of reviews can serve as evidence into the accuracy of defined philosophies for investment.

Industry collaboration and the fight against greenwashing

Greenwashing needs to be tackled by players across the investment value chain. Not-for-profits, academic institutions, and the media have played a big role in bringing this issue to light. Greenwashing must be dealt with at the following levels:

- Corporations, through robust disclosure practices

- ESG data providers, through transparency in methodologies and disclosure of any margins of error/uncertainty

- Investors, through appropriate fund naming and impact reporting

- Regulators, through comprehensive and uniform minimum standards for corporate disclosure, fund labeling, and fund reporting

- The scientific community, through constant monitoring and effective communication of evolving scientific recommendations.

Solution alignment to support regulation

Specifically at the regulatory level, we have seen significant interest among our clients to enhance existing indices and create new ones based on a comprehensive and rigorous interpretation of SFDR requirements. Over time, a clear and strong regulatory baseline should ensure a foundational alignment across ESG indices in the market.

As highlighted in our paper entitled ‘Sustainable investment fund labeling frameworks: An apples-to-apples comparison,’ country/market-specific ESG labels proliferating in European countries currently form a highly divergent and fragmented landscape. Ironically, alignment with European Union rules is often in itself a source of divergence since Sustainable Investment is not interpreted uniformly in the different pieces of EU legislation. The EU Taxonomy, when finalized, could change this.

A loophole at the level of any of these stakeholders can create confusion and misalignment in the market, ultimately leading to problematic capital misallocation. Considering current growth trends in sustainable investing in Europe, and in passive investment products such as ETFs, measures aiming to reduce the risk of capital misallocation will become crucial to facilitate the transition to a more sustainable financial system.

Industry collaboration and the fight against greenwashing

ESG is a short acronym belying a diverse range of topics. Greenwashers rely on the complexities of modern business to provide cover when they overstate their ESG commitment and to obfuscate the reality of their actions. Collaboration between a wide range of experts is essential when vetting ESG claims in order to take the full benefit of a diversity of professional viewpoints. Academics, lawyers, investors, risk professionals, data providers, managers, vendors are just some of the archetypes that can provide specialized knowledge to uncover greenwashing when it occurs. Only by holistically approaching the problem will the marketplace gain confidence that ESG claims are more than hot air.

The Integrity 2 ESG (I2E) certification draws on a diverse mix of internal resources and external partners to certify investment funds as either Integrated, ESG Focused, or ESG Impact. I2E worked closely with RepRisk to develop a “trust but verify” approach to certification. Using RepRisk’s rich data set, the I2E certification team is able to identify the risk in a given portfolio’s holdings and compare it to the portfolio’s documented ESG investment objectives. This data supports deep analysis across a variety of contexts. By working with our legal partners at Maples Group, we can understand how the portfolio risk is being reflected in regulator disclosures and assess their accuracy. Our internal team of investigators and investment practitioners use this data to form an objective, holistic view of the overall portfolio risk and compare it to a fund’s self-assessment. These are just two ways that collaboration among multiple parties allows I2E to more effectively combat greenwashing using multiple perspectives.

Solution alignment to support regulation

Regulatory compliance is always a challenging exercise with huge stakes for getting it wrong. It’s often not enough to know the printed words in a regulation; it’s also important to continually self-assess where an organization is against its industry peers as well as what the ongoing trends are. Internal resources at an organization often lack the expertise in specific regulations as well as the bandwidth to self-assess and identify issues. Trusted consortiums of outside groups working in tandem, such as in the Integrity 2 ESG certification, can provide a level of trust in the strength of a given ESG program as well as identify potential areas for improvement. Certification provides the dual benefits of making sure you are complying with the regulations as written as well as allowing you to benchmark against what peer institutions have in place due to the large number of entities reviewed by the I2E team. There is no substitute for rigorous analysis across the entire gamut of potential regulatory impacts by a team of experts.

IX. Supply chain, sovereign risk, and consumer perspectives

Value and supply chain

Another important use case that is gaining significant traction is supply chain and third-party risk management. With the German Supply Chain Act, vendors are introducing solutions that shed light on the indirect threats to a company’s ESG objectives via their supply chain. The ability to provide firms with the right data and metrics to perform extensive analysis on third-party relationships supports transparency on ESG exposures beyond operations that can be found in the depths of external entity relationships. Integration of ESG risk data into software that supports supply-chain management is a powerful component that highlights areas of ESG exposure, specifically linked to ESG issues that are important to an organization. The COVID-19 pandemic and the war in Ukraine are two recent events that have demonstrated how an ESG risk overlay can strengthen operational resilience across supply chains and other third-party relationships.

Sovereign data

Government and country risk assessments are an important consideration within ESG, especially with heightened geopolitical tensions, trade wars, and physical wars. Being able to understand sovereign risk from an ESG perspective provides insights on material ESG impacts on a country’s creditworthiness when undergoing credit risk assessments. This provides for a more holistic look at a country’s governance and commitment to sustainable development and increases the focus on good governance aligned with securing investment.

Consumers

Lastly, more will need to be done to close the gap between geopolitical influence, investments, corporates and consumers. The impact of financial investments on corporates and their link to ESG is evident, but in the future, the link between corporates and consumers will need to be addressed, with ESG data closing the gap on understanding consumer behaviors and how that behavior impacts funding.

In 2019, Mastercard introduced a carbon calculator that allows customers to track the carbon footprint of their purchases. Companies like Allbird and Unilever have introduced carbon labels on their products, with L’Oreal committing to doing the same by 2030. This is a great step forward in extending the reach of ESG data. Enabling consumers to manage their own ESG footprint more effectively with greater visibility on where their money is going and the impact they have on people and planet, is bringing ESG risk mitigation into the home setting, making sure everyone involved in the chain is doing their part in ensuring responsible business conduct.

X. Conclusion

Investment in and availability of ESG data continues to grow, and the evolving landscape presents opportunities for innovation in the field. It is important that datasets align with their marketed objectives to enable the industry to fully utilize the data in an efficient and meaningful manner. Emerging partnerships and collaborations demonstrate the ability for ESG data and technology to further add value in a multitude of settings, supporting firms across various business functions and strategic mandates.

Business partnerships represent the powerful capability of organizations to integrate data and technology to advance existing and develop new solutions. Partnerships bring together efficiency with effectiveness to solve for complex ESG issues, enable better decision-making aligned with responsible business practices, and empower the world of ESG data and technology.

Thank you to our partners

ICE is a Fortune 500 company that designs, builds and operates digital networks to connect people to opportunity. ICE provides financial technology and data services across major asset classes that offer customers access to mission-critical workflow tools that increase transparency and operational efficiencies. ICE operates exchanges, including the New York Stock Exchange, and clearing houses that help people invest, raise capital and manage risk across multiple asset classes. Their comprehensive fixed income data services and execution capabilities provide information, analytics and platforms that help customers capitalize on opportunities and operate more efficiently.

In partnership since 2020, ICE has been integrating ESG risk data from RepRisk into its ESG Reference Data service and more recently into its SFDR Principal Adverse Impact solution.

K2 Integrity is a premier financial crimes, risk, and regulatory advisory firm. With a focus on financial crimes risk management, investigations, monitoring, cybersecurity, and virtual asset advisory, K2 Integrity brings together deep subject-matter expertise with proprietary technology offerings to help clients creatively solve for today while preparing for tomorrow.

To certify to the market that ESG commitments are trustworthy and valid, Integrity 2 ESG’s certification has pioneered a first-of-its kind solution for the independent certification of ESG strategies for funds and fund managers. The firm’s dedicated ESG team embeds K2 Integrity’s global reputation, its risk and regulatory skills, and its proprietary framework and scoring methodology into the certification, adding long-term financial and reputational value.

In partnership since 2022, RepRisk provides K2 Integrity with access to its independent ESG risk data to incorporate into the process and analysis to help determine whether managers and funds are committed to ESG best practices and aligned to relevant standards and guidelines.

Part of the Deutsche Börse Group, Qontigo is a leading global provider of innovative index, analytics and risk solutions that optimize investment impact. Qontigo enables their clients — financial-products issuers, capital owners and asset managers — to deliver sophisticated and targeted solutions at scale to meet the increasingly demanding and unique sustainability goals of investors and asset owners worldwide. Their solutions, enhanced by both their collaborative, customer-centric culture, which allows them to create tailored solutions for their clients, and their open architecture and modern technology that efficiently integrate with their clients’ processes.

Qontigo and RepRisk signed a unique analytics partnership in 2022. Under the partnership, Qontigo enables solutions and access to RepRisk's ESG risk data via its Axioma Analytics suite of products and builds indices under its STOXX family of brands.

Copyright 2023 RepRisk AG. All rights reserved. RepRisk AG owns all intellectual property rights to this report. This information herein is given in summary form and RepRisk AG and/or the third party contributors to this report make no representation or warranty that any data or information supplied to or by it or them is complete or free from errors, omissions, or defects. Without limiting the foregoing, in no event shall RepRisk AG and/or the third party contributors to this report have any liability (whether in negligence or otherwise) to any person in connection with the information contained herein. Any reference to or distribution of this report must include a link to the content to provide sufficient context. The information provided in this presentation does not constitute an offer or quote for our services or a recommendation regarding any investment or other business decision, and is not intended to constitute or to be used as a substitute for legal, tax, accounting, or other professional advice. Please note that the information may have become outdated since its publication. Should you wish to obtain a quote for our services, please contact us.