Unpacking the EU Corporate Sustainability Reporting Directive (CSRD)

The Corporate Sustainability Reporting Directive (CSRD) is a key component of the EU's broader sustainable finance framework. It extends the scope and reporting requirements of the already existing Non-Financial Reporting Directive (NFRD) – a regulatory framework that mandates companies to report on their sustainability performance since 2018. The CSRD also replaced the NFRD upon its enforcement in January 2023 to meet the growing demand for transparency and mandate detailed disclosure of companies’ sustainability-related information.

The key elements of CSRD reporting include the concept of double materiality, which encompasses both how a company’s operations impact environmental, social, and governance (ESG) factors (impact materiality), and how these ESG factors, in turn, influence the company’s business operations (financial materiality). The CSRD also aims to ensure that there is adequate, publicly available information on the impacts, risks, and opportunities related to companies' operations and value chains. The CSRD’s requirements are phased in over time and its first phase of application started on January 1, 2024.

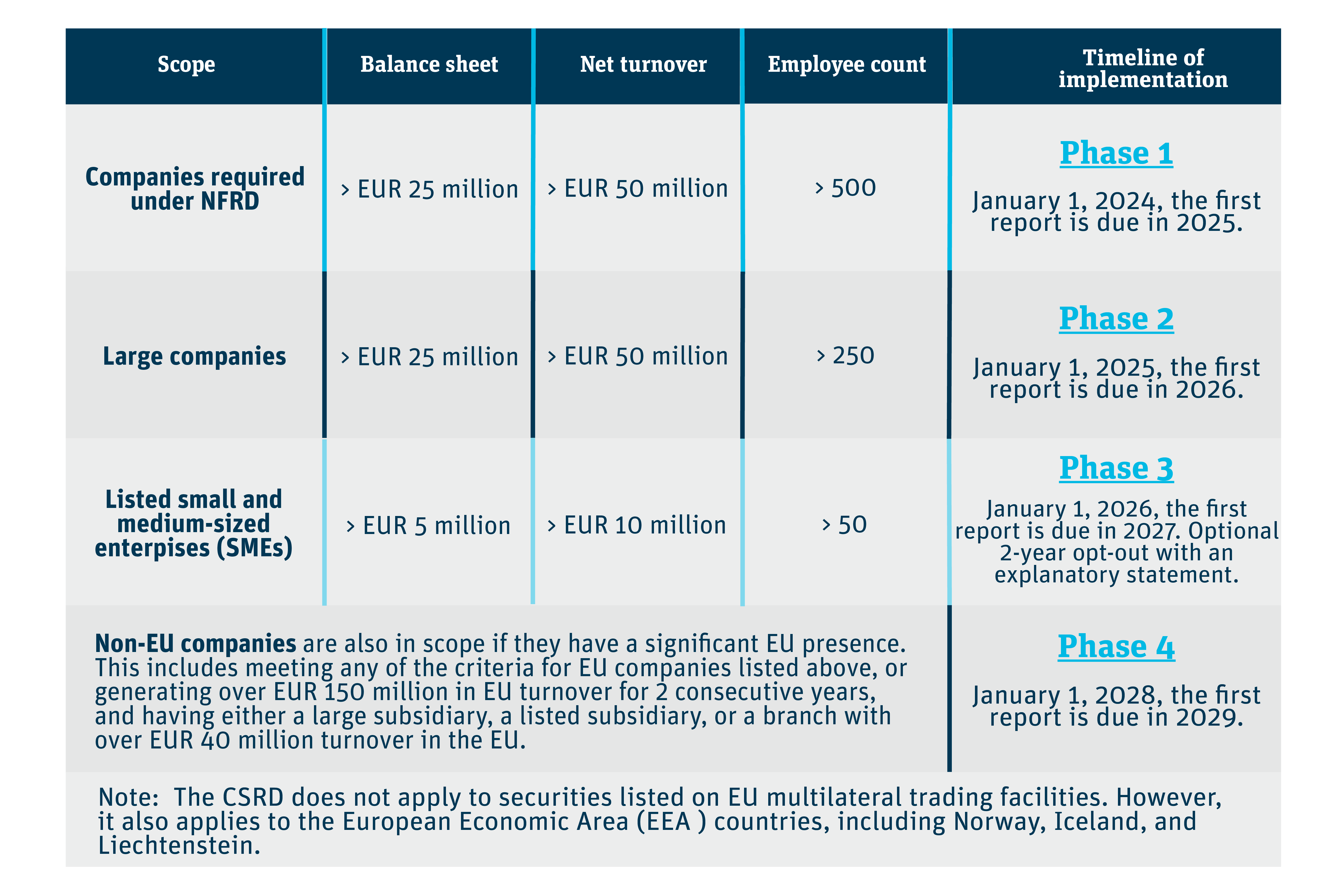

# I. Who’s in scope?

The CSRD applies to all large companies and those listed on EU-regulated markets, excluding micro-enterprises. This expansion covers nearly 50,000 companies, a significant increase from the 11,000 covered under the NFRD.

# II. What are the requirements?

- CSRD requires companies to disclose information on their sustainability strategy, including their business model, targets, and governance approach. It also mandates reporting on their sustainability implementation efforts, such as due diligence processes and impact mitigation measures, as well as their sustainability performance, including progress on targets and impacts on the environment, human rights, and social standards.

- Companies are required to file reporting information in the eXtensible Business Reporting Language (XBRL) format facilitating automated data processing and analysis for improved accuracy, efficiency, and comparability.

- To support the implementation of the CSRD, the European Financial Reporting Advisory Group (EFRAG) developed the European Sustainability Reporting Standards (ESRS). It entered into force on January 01, 2024, and aims to reflect the concept of double materiality and provide detailed guidelines, metrics, and disclosure requirements under the CSRD.

- While tailored to the European context, the ESRS is also designed to align with emerging global frameworks such as the Task Force on Climate-related Financial Disclosures (TCFD) and the International Sustainability Standards Board (ISSB) standards.

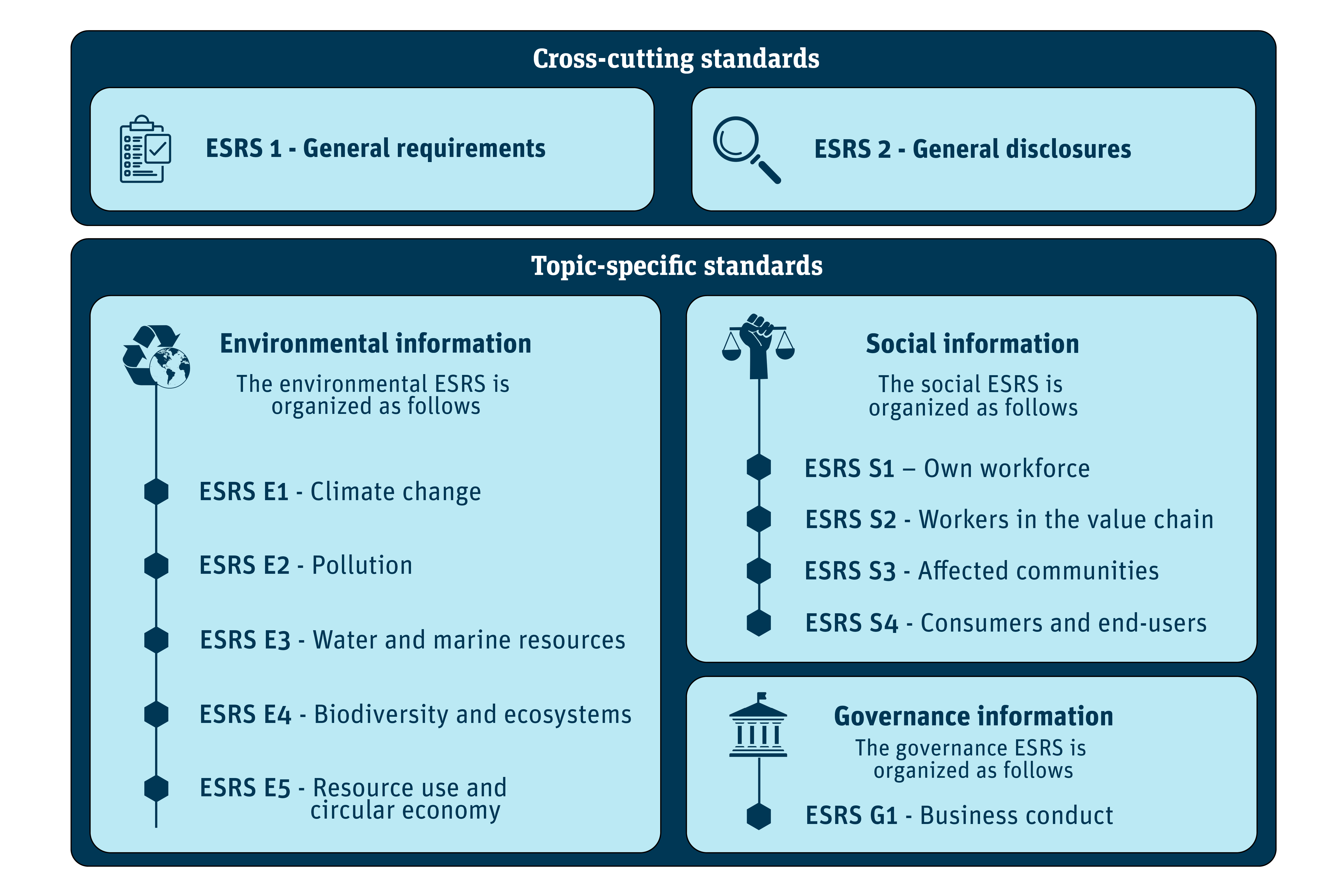

- It is categorized into two types of standards: the general standards called ESRS 1 and ESRS 2 which cover general disclosure requirements, and the topic-specific standards (ESRS E1-E5, ESRS S1-S4, and ESRS G1).

General requirements

#

ESRS 1 – General requirements

- It describes how to prepare and disclose sustainability-related information, including how to disclose information on an entity’s value chain, both upstream and downstream.

#

ESRS 2 – General disclosures

- It provides entities with a four-pillar structure for disclosing sustainability matters in the areas of good governance, strategy, impact, risk, and opportunity management, as well as metrics and targets. These four pillars are based on the TCFD and the ISSB standards.

- It also outlines the core elements of due diligence. Entities must disclose all steps of their due diligence process for sustainability matters, ensuring their disclosure encompasses their strategy, governance, risks, opportunities, business model, and sustainability impact.

Topic-specific standards

# Environmental information: ESRS E1 – ESRS E5

- Sets out environment-related metrics and disclosure requirements related to transition plans for climate change mitigation, climate-related scenario analysis, greenhouse gas (GHG) emission reduction targets, impact on biodiversity and ecosystems, and actions taken to protect and restore nature.

- The environmental ESRS is organized as follows:

1. ESRS E1 – Climate change

2. ESRS E2 – Pollution

3. ESRS E3 – Water and marine resources

4. ESRS E4 – Biodiversity and ecosystems

5. ESRS E5 – Resource use and circular economy

# Social information: ESRS S1 – ESRS S4

- Provides a framework for entities to report on social elements, such as work-related rights (e.g. human rights-related incidents), employees in their value chain, and others that may be affected by their operations or their products and services.

- These standards also describe how to disclose the gender pay gap and the total remuneration ratio.

- The social ESRS is organized as follows:

1. ESRS S1 – Own workforce

2. ESRS S2 – Workers in the value chain

3. ESRS S3 – Affected communities

4. ESRS S4 – Consumers and end-users

# Governance information: ESRS G1

- Outlines reporting obligations on an entity’s processes, procedures, and performance in relation to its business conduct (e.g. corporate culture, relationship with suppliers, business ethics and policies related to its business conduct, remuneration policies linked to sustainability matters, lobbying activities).

- Provides information on how to disclose the role of the administrative, management, and supervisory bodies:

1. ESRS G1 – Business conduct

A sector-specific ESRS is expected to be developed starting with eight priority sectors: oil and gas, mining, road transport, agriculture and fisheries, motor vehicles, energy production and utilities, food and beverages, and textiles, accessories, footwear, and jewelry. The ESRS for SMEs will also come at a later time. This expansion intends to facilitate the reporting requirements by tailoring them to the unique scale and complexity of each sector and company size, promoting proportionate and effective sustainability disclosures.

# III. How does CSRD align with the other sustainability regulations in the EU?

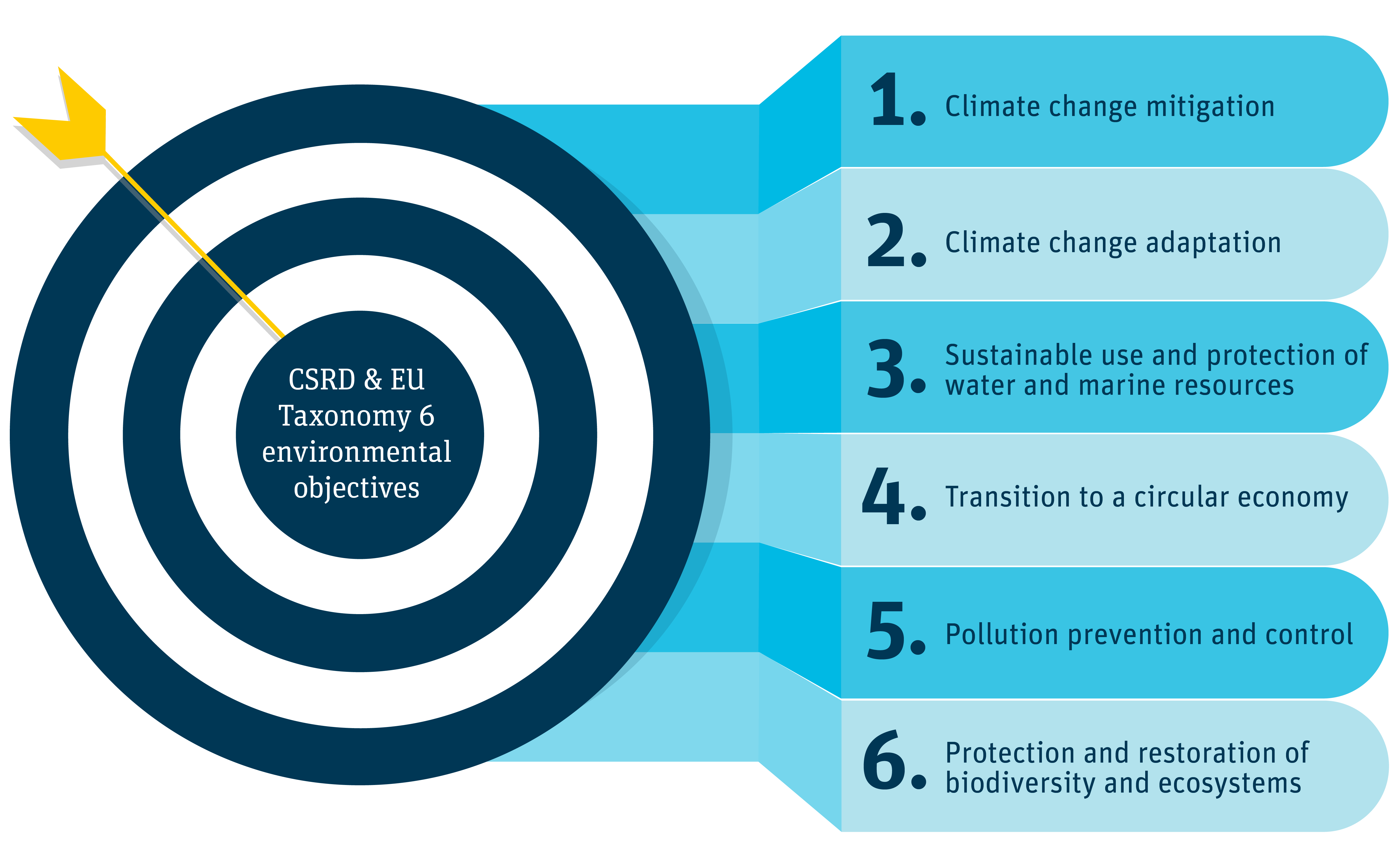

# 1. EU Taxonomy

The EU Taxonomy is a classification system established to clarify which economic activities are environmentally sustainable, aiming to prevent greenwashing and help investors make informed sustainable investment decisions. Both the CSRD and EU Taxonomy are guided by the same 6 environmental objectives:

- Climate change mitigation;

- Climate change adaptation;

- Sustainable use and protection of water and marine resources;

- Transition to a circular economy;

- Pollution prevention and control; and

- Protection and restoration of biodiversity and ecosystems.

The CSRD mandates companies to report on their sustainability performance, including the alignment of their activities with the EU Taxonomy. This alignment is essential to achieving the EU's ambitious climate and environmental objectives outlined in the European Green Deal.

# 2. Corporate Sustainability Due Diligence Directive (CSDDD)

The CSRD and the CSDDD are two EU regulations that work in tandem to promote sustainable business practices. The CSRD mandates that companies report on their due diligence processes, which are required under the CSDDD. This alignment creates a comprehensive framework that covers both the actions companies must take to address their impacts (CSDDD) and the transparent disclosure of those actions (CSRD). The alignment provides investors with reliable and comparable information on companies' sustainability performance, including their due diligence efforts. This increases investor confidence and supports the flow of capital towards sustainable investments.

# 3. Sustainable Finance Disclosure Regulation (SFDR)

The CSRD and SFDR work in tandem to increase transparency and comparability of sustainability information. While the CSRD focuses on corporate reporting, the SFDR mandates financial market participants and financial advisors to disclose how they integrate sustainability risks and impacts into their investment decisions and advisory services. The alignment of CSRD and SFDR is essential for creating a robust and effective sustainable finance ecosystem in the EU.

Want to learn more about RepRisk solutions for CSRD?

Contact your Account Manager or our Client Services Team (support@reprisk.com)

Copyright 2024 RepRisk AG. All rights reserved. RepRisk AG owns all intellectual property rights to this report. This information herein is given in summary form and RepRisk AG and/or the third party contributors to this report make no representation or warranty that any data or information supplied to or by it or them is complete or free from errors, omissions, or defects. Without limiting the foregoing, in no event shall RepRisk AG and/or the third party contributors to this report have any liability (whether in negligence or otherwise) to any person in connection with the information contained herein. Any reference to or distribution of this report must include a link to the content to provide sufficient context. The information provided in this presentation does not constitute an offer or quote for our services or a recommendation regarding any investment or other business decision, and is not intended to constitute or to be used as a substitute for legal, tax, accounting, or other professional advice. Please note that the information may have become outdated since its publication. Should you wish to obtain a quote for our services, please contact us.